The 7 Best ERC Companies For Getting Your ERC Funds

Read More Jul 10, 2023 Filed under: Accounting, Bookkeeping, Invoicing, Small Business

💳 Save money on credit card processing with one of our top 5 picks for 2022

Expert Analyst & Reviewer

UPDATED

If you are wondering not only what a merchant category code (MCC) is but also what it means for your business, you’re in the right place. Credit card processing can be a confusing and overwhelming topic, but when you become familiar with basic terms, everything becomes easier to understand. And when you understand how MCC codes fit into the larger landscape of payment processing, you can make better decisions for your business, too!

To demystify what your MCC code is and how it affects your business, keep reading.

Table of Contents

What is an MCC code, and why do you need to know about it for your business? A merchant category code, or MCC, is a four-digit number that indicates your line of business and the types of goods or services you provide to your customers.

Originally developed to simplify accounting for the year-end 1099 tax form reporting, the MCC code is now a critical piece in the payments landscape. While the International Organization for Standardization (ISO) sets the MCC codes and meanings, credit card processors nowadays assign the codes to merchants. These credit card merchant codes are then used by acquiring banks and payment service providers to set fees, assess risk, and more. Keep in mind that each card network — Visa, Mastercard, Discover, and American Express — each has its own list of MCCs. While they are largely similar, there might be some specific differences for certain types of businesses.

As the uses for merchant category codes have increased, so has their overall importance. Since your MCC code affects how credit card processors identify your company, knowing how you tend to be categorized can be helpful when you’re comparison shopping for rates.

You should also know that many payment services companies use MCC codes to identify and mark “prohibited industries” that they will not take on as customers. If you fall into one of these high-risk categories, you may need to look at providers that specialize in payment services to high-risk industries.

Additionally, some providers may only offer specialized features to businesses with specific MCCs, such as the option to charge a convenience fee for credit card purchases.

Your MCC code is something that usually exists quietly behind the scenes once your business gets going. You’re probably not going to find it on your merchant statement, and if you don’t know how to find your merchant category code or do a little digging, you may not even know what it is at all!

Here’s a quote from Trace Wendell, VP of Sales and Operations at Dharma Merchant Services, that sums it up best:

The important thing to remember is that the MCC code is chosen by the processor during the application process. It cannot be chosen by the merchant. Certainly, some merchants can request a specific MCC. But, they will only get it if they qualify for it.

When you’re applying for a merchant account, it certainly is beneficial to you to understand what types of MCCs may apply to your business. However, there are specific criteria to qualify for these MCCs. Some merchants may blur the line between categories but don’t quite make the cut for the lower interchange rates of a particular merchant category code because of the particulars of their day-to-day business, and that’s okay.

If you want to know your specific code, we recommend contacting your processor and asking them to find out what MCC code has been assigned to your business.

Each card network maintains its own MCC code list. Your best bet is always to go right to the networks to find their lists; some merchant account providers or other financial organizations post merchant category code listings as well.

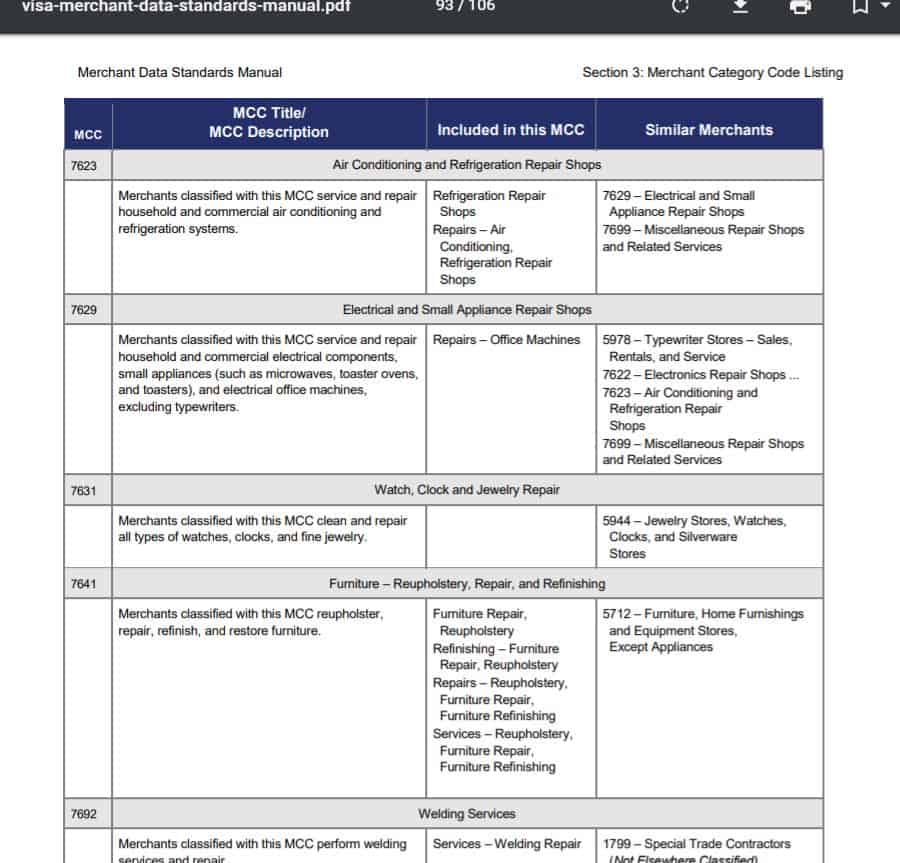

A great source of information about merchant categories and related policies and guidelines is the Visa Merchant Data Standards Manual. Here you can see that even under a general blanket (e.g., repair shops), the codes get a lot more specific depending on the products and services a merchant provides.

Since your MCC code represents the “predominant business activity of the merchant,” it can influence payment processing in a few different ways:

Yes, for certain types of organizations. As touched on above, merchant account providers utilize the MCC code to identify what type of business you’re in to determine interchange rates. Nonprofit organizations, healthcare, education, and B2B businesses generally enjoy lower interchange rates than other types of businesses.

Visa and Mastercard both offer lower interchange rates to “emerging markets” — that is, businesses that historically haven’t accepted credit cards as their predominant form of payment. That includes healthcare and education as well as government organizations, utilities, and even insurance sales.

Of course, specific requirements apply to be qualified for these MCC codes. That’s because, ultimately, you can request a review for certain codes, but the credit card processor assigns them based on specific criteria.

For more information on special interchange rates that businesses can qualify for with the right MCC code, check out our complete guide to B2B credit card processing.

It’s rare for transactions to be declined due to MCC codes but not unheard of. When it happens, it will usually be due to a restriction over the type of credit card your customer hands you.

Some customers may have cards that have restricted usage: for example, an EBT card or health care savings account card. EBT cards and health care cards are only authorized for specific types of commerce. If the customer tries to use them for any unauthorized purpose, the card may be declined and show an MCC code error.

Most businesses probably won’t run into serious issues with their MCC Codes, but there are times when it’s worth looking into updating your code with your payment services company. Instances in which you may want to push the issue include:

MCC codes are a critical component of every business when it comes to accepting credit cards. They are decided by credit card processors at the start of the application process and indicate what type of business you have and what products or services you provide.

Understanding how this code affects you can help you decide whether or not to register as a nonprofit or request that additional MCC codes apply to an expanding part of your business. Beyond reaching out to your credit card processor, however, there isn’t much you can do as a business owner to make the final decision about your MCC code, as it’s based on specific criteria identified by the credit card processor at the time of your application.

Need more information on credit card processing? We have a world of resources waiting for you. Start by checking out our article on small business credit card processing companies not only to see some top picks but also to learn what to look for when you’re shopping around.

We've done in-depth research on each and confidently recommend them.

We've done in-depth research on each and confidently recommend them.

Let us know how well the content on this page solved your problem today. All feedback, positive or negative, helps us to improve the way we help small businesses.

Give Feedback

Help us to improve by providing some feedback on your experience today.

The vendors that appear on this list were chosen by subject matter experts on the basis of product quality, wide usage and availability, and positive reputation.

Merchant Maverick’s ratings are editorial in nature, and are not aggregated from user reviews. Each staff reviewer at Merchant Maverick is a subject matter expert with experience researching, testing, and evaluating small business software and services. The rating of this company or service is based on the author’s expert opinion and analysis of the product, and assessed and seconded by another subject matter expert on staff before publication. Merchant Maverick’s ratings are not influenced by affiliate partnerships.

Our unbiased reviews and content are supported in part by affiliate partnerships, and we adhere to strict guidelines to preserve editorial integrity. The editorial content on this page is not provided by any of the companies mentioned and has not been reviewed, approved or otherwise endorsed by any of these entities. Opinions expressed here are author’s alone.